In Singapore, corporate transparency is not optional. One of the key compliance requirements introduced under the Companies Act is the Register of Registrable Controllers (RORC). For SMEs and foreign-owned companies, this obligation is often misunderstood or overlooked, yet non-compliance can expose directors and shareholders to fines and regulatory scrutiny.

In simple terms, the register of registrable controllers identifies the individuals or entities that ultimately own or control a company in Singapore. It is a core governance requirement enforced by ACRA and applies to most locally incorporated companies, regardless of size or activity level.

This article explains what a registrable controller is, why the RORC matters, who is responsible for maintaining it, and the practical risks associated with getting it wrong.

Understanding the Meaning of a Registrable Controller

Definition of a Registrable Controller

A registrable controller is an individual or legal entity that has a significant interest in, or significant control over, a company incorporated in Singapore.

Under the Companies Act, this goes beyond who is listed on the share register. The focus is on ultimate ownership and control, including indirect arrangements and nominee structures.

In practice, a registrable controller is the person or entity that truly “calls the shots”, even if they do not appear on official shareholding documents.

Who Qualifies as a Registrable Controller?

A person or entity generally qualifies as a registrable controller if they:

- Hold more than 25% of the company’s shares or voting rights, whether directly or indirectly; or

- Exercise significant influence or control over the company’s decisions, management, or policies.

This can include foreign parent companies, founders who hold shares through nominees, or individuals with contractual control rights.

What Is the Register of Registrable Controllers?

Purpose of the Register of Registrable Controllers

The register of registrable controllers is an internal statutory register that records details of the company’s registrable controllers.

Its primary purpose is to:

- Enhance corporate transparency

- Prevent the misuse of companies for money laundering or tax evasion

- Allow regulators such as ACRA and law enforcement agencies to identify beneficial owners quickly

The register is not publicly available, but it must be accurate, up to date, and readily accessible to authorities upon request.

Why the Register of Registrable Controller Is Important

From a compliance perspective, the RORC is as critical as maintaining proper accounting records or filing Annual Returns.

Based on JDT’s experience supporting foreign founders, RORC issues often surface during:

- ACRA inspections

- Bank account opening or reviews

- Due diligence for investments, M&A, or audits

As Joe Tan, Managing Partner of JDT, notes:

“Many directors assume that listing shareholders is enough. In reality, ACRA looks through nominee and holding structures. If the register of registrable controllers is incomplete, the company and its officers are exposed.”

Who Is Required to Maintain a Register of Registrable Controller?

Companies Required to Keep a Register

Most companies incorporated in Singapore are required to maintain a RORC, including:

- Private limited companies

- Foreign-owned subsidiaries incorporated in Singapore

- Dormant companies

This applies regardless of revenue, employee headcount, or whether the company is actively trading.

Companies engaging corporate secretarial services for incorporation are typically advised to set up the register at the point of incorporation, but it must be maintained throughout the company’s life.

Entities Exempted from the Requirement

Certain entities are exempt, including:

- Public companies listed on approved exchanges

- Singapore financial institutions regulated by MAS

- Companies wholly owned by the Singapore Government

These exemptions are narrow and strictly defined under the Companies Act.

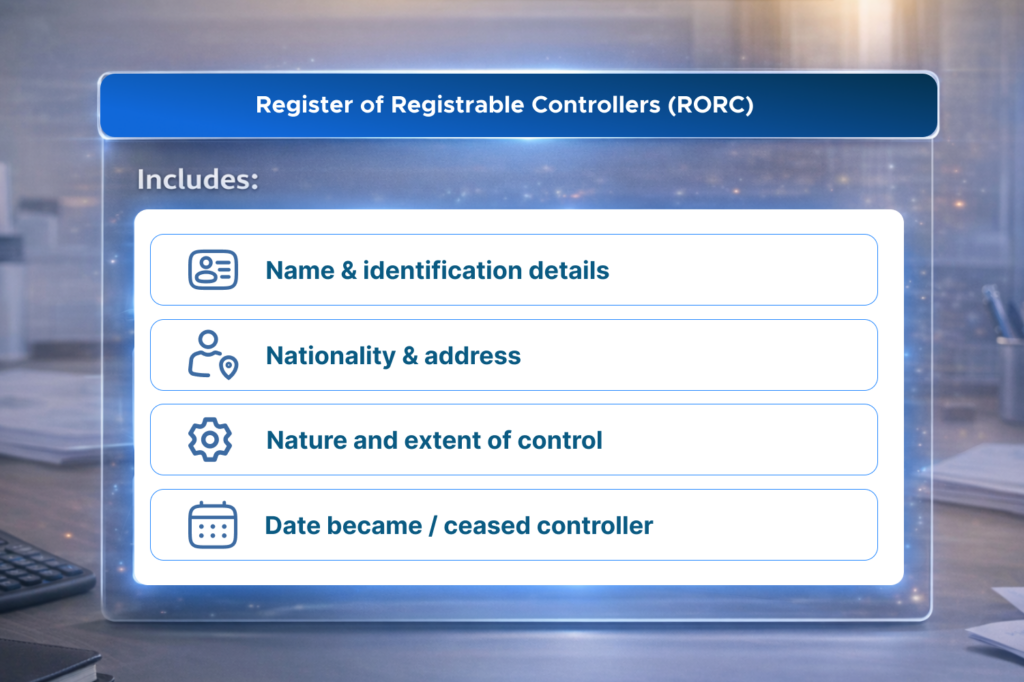

Information Included in a Register of Registrable Controller

Personal Details of a Registrable Controller

For individual registrable controllers, the register must include:

- Full name

- Nationality

- Identification number (NRIC or passport)

- Residential address

For corporate controllers, details such as the entity name, registration number, and registered office address are required.

Nature and Extent of Control

The register must clearly state how the controller exercises control, for example:

- Shareholding percentage

- Voting rights

- Contractual or constitutional rights

This is where many companies fall short, particularly when control is exercised indirectly through layers of ownership.

Dates of Becoming and Ceasing a Registrable Controller

Companies must also record:

- The date the person or entity became a registrable controller

- The date they ceased to be one (if applicable)

These dates are important for demonstrating compliance during audits or regulatory reviews.

How to Identify a Registrable Controller

Ownership and Shareholding Thresholds

The most straightforward test is ownership. A registrable controller usually holds:

- More than 25% of issued shares; or

- More than 25% of voting power

This includes indirect ownership through holding companies or trusts.

Significant Influence or Control Explained

Even without meeting shareholding thresholds, a person may still be a registrable controller if they can:

- Appoint or remove directors

- Influence financial or operating decisions

- Veto key resolutions

Doreen Yip, Executive Director, Financial Outsourcing & Business Advisory at JDT, highlights that “control is not always visible on paper. We often see founders retain control through shareholder agreements, which must still be reflected in the RORC.”

How to Maintain and Update the Register of Registrable Controller

Where the Register Should Be Kept

The RORC must be kept at:

- The company’s registered office; or

- The office of its appointed corporate secretary in Singapore

It must be available for inspection by ACRA upon request.

When Updates Are Required

Companies must update the register within two business days of becoming aware of any change, such as:

- New registrable controllers

- Changes in ownership or control

- Controllers ceasing to have control

Delays often occur when changes are not communicated internally, especially in foreign-owned structures.

Record-Keeping Best Practices

Best practices include:

- Reviewing the RORC annually before AGM and Annual Return filings

- Aligning the register with shareholder agreements and group charts

- Ensuring directors understand their personal liability

Maintaining the register alongside other statutory records reduces the risk of inconsistencies during audits or compliance checks.

Penalties for Failing to Maintain a Register of Registrable Controller

Common Compliance Mistakes

Common issues JDT encounters include:

- No register maintained at all

- Register created but never updated

- Nominee arrangements not disclosed

- Inaccurate or incomplete control descriptions

These errors are often unintentional but still penalised.

Legal Consequences and Fines

Failure to maintain a proper RORC is an offence under the Companies Act. Penalties may include:

- Fines of up to SGD 5,000 per offence

- Ongoing fines for continuing breaches

- Personal liability for directors and officers

In serious cases, compliance failures can also affect banking relationships and future corporate transactions.

Register of Registrable Controller vs Other Corporate Registers

Difference Between Registrable Controller and Shareholders

Shareholders are those whose names appear on the share register. Registrable controllers are those who ultimately own or control the company.

A shareholder may not be a registrable controller, and a registrable controller may not appear as a shareholder at all.

Register of Registrable Controllers vs Register of Directors

The register of directors records who manages the company. The RORC records who controls it.

Foreign founders commonly use nominee directors; however, this does not exempt them from the obligation to disclose the true controllers.

Frequently Asked Questions About Registrable Controller

Can a Company Have More Than One Registrable Controller?

Yes. A company can have multiple registrable controllers, particularly where ownership or control is shared.

All qualifying controllers must be recorded in the register.

Does a Nominee Director Count as a Registrable Controller?

Not necessarily. A nominee director is only a registrable controller if they also meet the ownership or control criteria.

In most cases, the appointing shareholder or parent entity is the registrable controller.

How Often Should the Register Be Reviewed?

At a minimum, the register should be reviewed:

- Annually before filing the Annual Return with ACRA

- Whenever there is a change in ownership, control, or group structure

Regular reviews reduce the risk of last-minute issues during audits or due diligence.

Maintaining a compliant register of registrable controllers (RORC) is not a formality. It is a legal obligation that reflects how well a company understands and manages its governance responsibilities.

If you are unsure whether your RORC is accurate, or if your ownership structure has changed since incorporation, it may be prudent to conduct a compliance review. The company registration services team at JDT regularly assists SMEs and foreign founders with registrable controllers requirements in Singapore, from incorporation through ongoing corporate secretarial support, complemented by our corporate advisory services for more complex governance and structuring matters.

To discuss your obligations or arrange a register review, you may contact us for a calm, professional consultation, or learn more about JDT and how we support long-term, low-risk corporate compliance.